What is marginal VaR?

By Gabriel Cooper

What is marginal VaR?

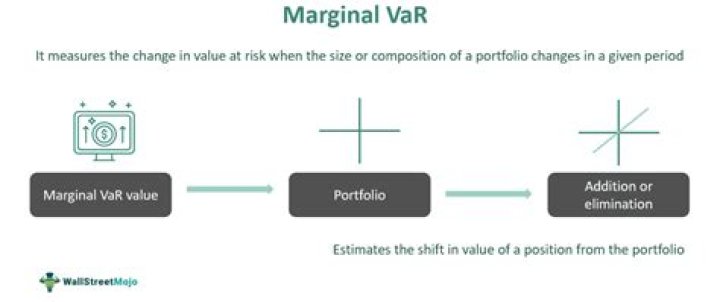

Marginal VaR refers to the additional amount of risk that a new investment position adds to a firm or portfolio. Marginal VaR allows risk managers to study the effects of adding or subtracting positions from an investment portfolio.

How do you calculate marginal contribution to risk?

Marginal contribution to risk= To find the marginal contribution of each asset, take the cross-product of the weights vector and the covariance matrix divided by the portfolio standard deviation. Now multiply the marginal contribution of each asset by the weights vector to get total contribution.

How do you calculate iVaR?

According to the most commonly used formula, IVaR is approximately equal to the current VaR multiplied by the beta coefficient of the candidate asset.

What is the component VaR?

Component VaR (CVaR) Component VaR for the i-th asset is nothing but the product of Marginal VaR and the value of the i-th asset. Component VaR has the useful property that it adds up to the dollar VaR of the portfolio, that makes life very easy from a risk disaggregation perspective.

What is MVaR in finance?

The marginal value at risk (MVaR) method is the amount of additional risk that is added by a new investment in the portfolio. MVaR helps fund managers to understand the change in a portfolio due to the subtraction or addition of a particular investment.

What is contribution VaR?

The contribution of a position or a sub portfolio to the total VaR is measured by value at risk contribution (VaRC). VaRC is the additive decomposition of the total portfolio VaR and is calculated and reported both at portfolio level as well as single deal level.

What is marginal risk contribution?

Marginal risk contributions are the incremental risks due to a new facility or a new sub-portfolio added to an existing portfolio. They are risk differences before and after inclusion of a new facility or a new sub-portfolio.

What is contribution to variance?

The sequential contribution to variance technique calculates how much more of the variance in an output is explained by adding each of a sequence of inputs to the regression model. The selection of the variables and the order in which they are added is determined by the stepwise regression procedure.

What is Icvar?

The Indian Council of Agricultural Research (ICAR) is the apex body for coordinating, guiding, and managing research and education in agriculture in the entire country under the aegis of DARE, Ministry of Agriculture and Farmers Welfare.

What is a VaR number?

Value at risk (VaR) is a statistic that quantifies the extent of possible financial losses within a firm, portfolio, or position over a specific time frame. One can apply VaR calculations to specific positions or whole portfolios or use them to measure firm-wide risk exposure.

What is individual VaR?

The VaR of an individual position in a portfolio is known as the individual VaR. For a given confidence level and a time period, VaR is the largest possible loss. Value At Risk (VaR) is one of the most important market risk measures. In short, VaR is the maximum loss for a given confidence level.

What is VaR calculation?

Value at Risk (VAR) calculates the maximum loss expected (or worst case scenario) on an investment, over a given time period and given a specified degree of confidence. We looked at three methods commonly used to calculate VAR.