What is Macaulay duration example?

By Daniel Avila

What is Macaulay duration example?

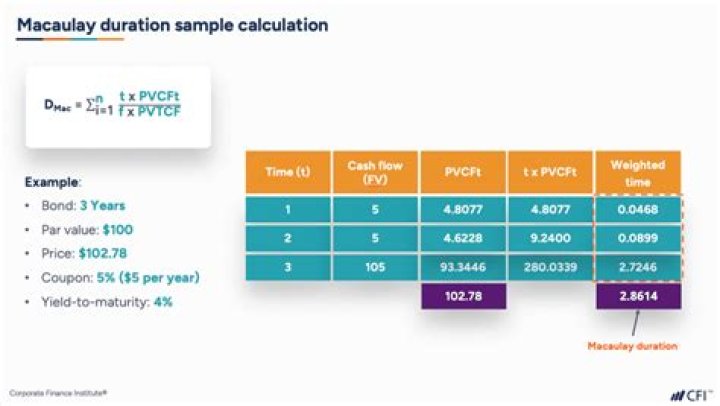

Example: Consider a 2-year coupon bond with a face and redemption value of $100 and a coupon rate of 10% per annum payable semiannually and a yield to maturity of 12% per annum compounded semiannually. Find the Macaulay Duration. The Macaulay Duration is 3.7132 semiannual periods or 1.86 years.

What is modified duration example?

For example, assume bank A and bank B enter into an interest rate swap. The modified duration of the receiving leg of a swap is calculated as nine years and the modified duration of the paying leg is calculated as five years. The resulting modified duration of the interest rate swap is four years (9 years – 5 years).

How do you convert modified duration to Macaulay duration?

To find the modified duration, all an investor needs to do is take the Macaulay duration and divide it by 1 + (yield-to-maturity / number of coupon periods per year). In this example that calculation would be 2.753 / (1.05 / 1), or 2.62%.

How is Macaulay duration used?

The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price. Macaulay duration is frequently used by portfolio managers who use an immunization strategy.

What is the difference between duration and modified duration?

1. Duration or Macaulay Duration refers to measurement of weighted average time before having the cash flow, while Modified Duration is more on the percentage change in price in terms of yields.

What is the modified duration of a zero coupon bond?

the modified duration of a zero-coupon bond is the time til maturity. for example, the modified duration of a 10-year, zero-coupon bond is ten years. if you purchase the above bond when it is halfway to maturity, the modified duration is half that, or equal to five years.

What is Macaulay duration in mutual funds?

Macaulay Duration is a measure of how long it takes for the price of a bond to be repaid by its internal cash flows. It measures the change in the value of a fixed income security that will result from a 1% change in the interest rate.

What is modified duration in MF?

Modified duration is simply the price sensitivity of a bond to changes in yields or interest rates. So if the modified duration of a bond is 10 years and interest rates go down by 1%, then the bond price will increase by 10%.

How do you do Macaulay duration in Excel?

The formula used to calculate a bond’s modified duration is the Macaulay duration of the bond divided by 1 plus the bond’s yield to maturity divided by the number of coupon periods per year. In Excel, the formula used to calculate a bond’s modified duration is built into the MDURATION function.

Why we use modified duration?

The modified duration provides a good measurement of a bond’s sensitivity to changes in interest rates. The higher the Macaulay duration of a bond, the higher the resulting modified duration and volatility to interest rate changes.

What is Macaulay duration of a zero coupon bond?

The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount.

What is the difference between modified and effective duration?

The difference between modified duration and effective duration is that modified duration assumes that the cash flows won’t change, while effective duration allows that the cash flows might change.

What does Macaulay duration mean?

What is the ‘Macaulay Duration’. The Macaulay duration is the weighted average term to maturity of the cash flows from a bond.

What is the formula for modified duration?

The modified duration is an adjusted version of the Macaulay duration, which accounts for changing yield to maturities. The formula for the modified duration is the value of the Macaulay duration divided by 1, plus the yield to maturity, divided by the number of coupon periods per year.

What does modified duration mean?

Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Modified duration follows the concept that interest rates and bond prices move in opposite directions.